Sukanya Samrudhi Yojana is currently paying interest at the rate of 7.6% per annum

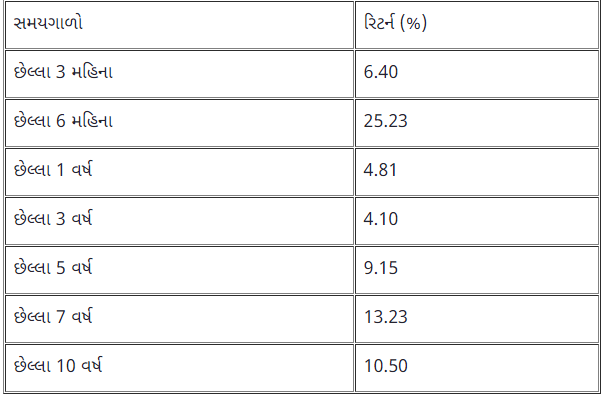

The HDFC Children’s Gift Fund has returned more than 10% in the last 10 years

Mutual funds are being considered as a good investment option in our country. Many funds have given good returns in the last few years. In such a situation many people are confused as to whether to invest from Sukanya Samrudhi Yojana or mutual fund for their own daughter. Today we are going to tell you about both these schemes so that you can choose the right option according to you.

Sukanya Samrudhi Yojana

Under Sukanya Samrudhi Yojana, an account can be opened after the birth of a child at the age of 10 years. This scheme can be opened anywhere in a bank or post office. Sukanya Samrudhi Yojana is currently offering interest at the rate of 7.6% per annum.

An account can be opened for Rs.250

An account can be opened for Rs 250. Under Sukanya Samrudhi Yojana, an account can be opened only after the birth of a child at the age of 10 years. The account will mature after the daughter turns 21 or the girl gets married and you will get full payment with interest.

The account can also be closed after 5 years

The account can also be closed up to 5 years after opening. It is allowed to close if a serious illness occurs or if the account is being closed for any other reason. But the interest on it will be paid according to the savings account.

Half the money can be withdrawn when the daughter turns 18

Up to 50% of the cost for higher education of a child after the age of 18 can be withdrawn in the account of Sukanya Samrudhi Yojana. To open an account it is necessary to give birth certificate of daughter. Proof of identity and address of the child and parents must be provided. This account can be transferred anywhere in the country. This facility is available to the account holder if he / she shifts from the original place of account opening to another place. There is no charge for this. If the account is being closed before the completion of 21 years, the account holder has to give an affidavit that the daughter is not less than 18 years of age at the time of closing the account.

Benefit from tax exemption

A maximum of Rs 1.5 lakh can be deposited under Sukanya Samrudhi Yojana in the current financial year. The benefit of tax exemption under Section 80C of the Income Tax Act can also be availed on deposits under Sukanya Samrudhi Yojana.

Mutual funds

Mutual funds can give higher returns

Sukanya Samrudhi Yojana may have a tax benefit but you get a fixed interest in it, in which you cannot earn more than that. Considering the problem of rising inflation over time, investing in an equity mutual fund may prove to be good for the future of children. Equity Mutual Funds can choose any option as required from Index Fund, Large Cap Fund, and Mid Cap Fund. An investment plan in an equity fund can be selected according to the risk profile. According to experts, investing in an equity mutual fund is the best option for an investment of 10 years or more.

Child Mutual Fund option is available

Child mutual funds are also good for the future of children. However, long term investment is better for him. Returns from child mutual funds are also capable of countering the problem of inflation. However, it is not possible to invest only in the name of the child in the fund with which the child is associated. Such plans are especially tempting to invest in the name of children. However, there are also some good plans out there. But parents can also look at other mutual funds.

Top Children’s Plan Returns

HDFC Children’s Gift Fund

Value of 10 thousand monthly SIP in 10 years: Rs

Expense ratio: 2.06% (November 5, 2020)

Minimum investment: Rs

Minimum SIP: Rs.500

ICICI Prudential Child Care Fund

{kind=link}

{kind=link}

Monthly SIP of 10 thousand has a value of Rs. 18.23 lakhs in 10 years

Expense ratio: 2.52% (November 5, 2020)

Minimum investment: Rs

Minimum SIP: Rs.500

UTI Children’s Career Fund Investment Plan

Value of 10 thousand monthly SIP in 10 years: Rs

Expense ratio: 2.76% (November 5, 2020)

Minimum investment: Rs

Minimum SIP: Rs.500

Source: Value Research and groww.in.

Where to invest in Sukanya Yojana or Mutual Fund?

Both schemes have their own merits and demerits. If you can take a little risk then investing in a mutual fund will be right for you. Also, if you want to invest in a place where your money is safe and you get a good return without taking any risk, then Sukanya Yojana will be good for you. In addition, if you want to invest to save income tax, you can invest in Sukanya Yojana. It has the benefit of tax exemption